Options for Charitable Giving

Winston Churchill once said, “We make a living by what we get. We make a life by what we give.” The wealth created in Silicon Valley allows many in the tech industry to follow that maxim and give to the causes that mean the most to them. This primer is intended to help our clients and others make their giving more impactful and easier.

For many, the simplest way to give is direct cash donations to charities. This encompasses everything from the money put in a collection plate or Salvation Army bucket to annual checks to your alma mater. If you are among the roughly two thirds of taxpayers who take the standard deduction, then you do not even have to worry about keeping records of your donations. However, as household wealth and giving rises, there are other factors to consider that may make an approach other than direct cash donations more attractive, including:

Tax planning and management, for the benefit of both you and the organizations to which you give;

Having the flexibility to gift assets other than cash, such as stock or real estate, for tax or liquidity purposes;

Retirement planning, including giving designed to provide income from donated assets; and

Having the ability to extend your philanthropy beyond your lifetime

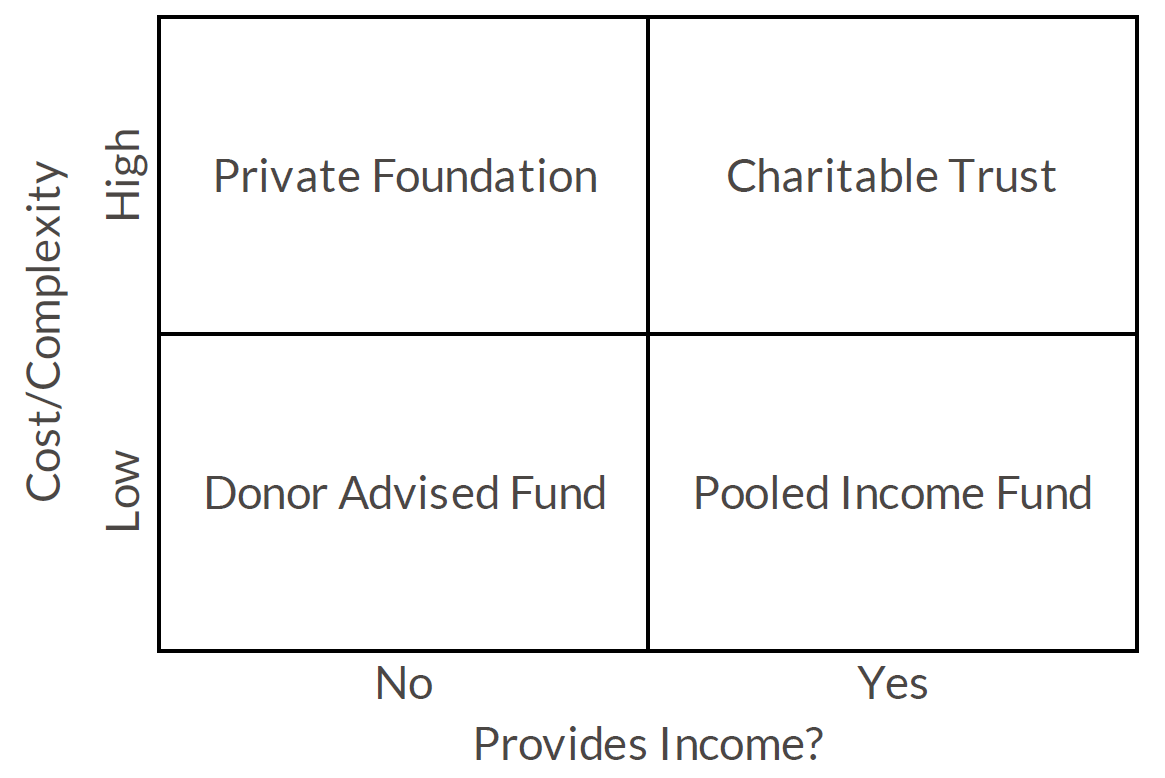

In general, the structures that exist for dealing with some, or all, of the above issues do so by separating the timing of the charitable donation by the individual and the gifting to the charitable cause or organization. By decoupling those events, donors have an increased ability to manage their taxes, increase their giving via investment performance and develop long-term giving strategies, which may extend beyond their lifetimes. The four structures we highlight here are: Donor Advised Funds (DAF); Pooled Income Funds (PIF); Charitable Trusts; and Private Foundations. The four types of structures differ mainly in terms of their cost/complexity and whether they can provide an income stream to the donor, as shown in the figure below.

One way to think about the cost/complexity dimension is that DAF and PIF structures closely resemble aspects of private foundations and charitable trusts, respectively, at a lower cost because the establishment and record keeping is outsourced to a third party. In exchange, those structures lack some of the flexibility and customization of foundations and trusts. While not a hard and fast rule, we typically advise clients that $1 million of assets is the threshold at which the more costly/complex structures are worthy of consideration. Although these four structures have key differences, it is important to keep in mind one they all have in common – funds that you contribute into the structure are no longer available to use for other purposes.

Donor Advised Funds

A donor advised fund (or DAF) is a separate account maintained by a sponsoring charitable organization. Once a donor contributes to the account, the sponsoring organization has legal control over it, though the donor retains advisory privileges with respect to both how the assets are invested and how the funds are granted. For tax purposes, grants to the DAF are tax deductible but grants to charities from the DAF are not.

In addition to being able to deduct DAF contributions immediately while granting them to the charities of your choice over time, another key advantage of donor advised funds is that the funds can appreciate tax-free. Other benefits of a DAF include greater ease of contributing appreciated stock (thereby avoiding capital gains taxes) and simplified record keeping. Some DAF providers can accept assets other than cash and publicly traded securities, including property and privately held stock.

Pooled Income Funds

Pooled income funds are tax-exempt charitable trusts that provide donors with an immediate tax deduction and a lifetime income stream. A PIF is a comingled trust and donors receive ownership stakes in the fund proportional to their contributions. The contributions are invested in various managed portfolios and the donor receives an annual payment based on the earnings of the portfolio. Note that the income stream is not guaranteed and can vary over time. Upon the donor’s death, the charity receives the donor’s share in the fund. Like DAFs, policies vary from fund to fund in terms of the types of assets that can be contributed.

Private Foundations

Private foundations are non-profit organizations established by the donor. The additional flexibility provided by a foundation compared to a DAF comes in two main forms – where contributions can be made and you and your family’s involvement. Because the foundation is itself a non-profit, contributions can go to entities and individuals that are not organized as non-profits themselves. Unlike a DAF, where you and your family are limited to an advisory role with respect to the disbursement of funds, a foundation can employ family members, subject to stringent IRS rules.

In exchange for this flexibility, foundations have additional costs with respect to both their establishment and ongoing administration. Unlike DAFs, foundations must distribute at least 5% of the income from its investments every year. There are also various tax aspects of foundations that are less attractive than DAFs, including lower limitations on deductions, how certain types of gifts are valued (cost versus fair market value) and the foundation’s requirement to pay excise taxes on investment income of up to 2% per year.

Charitable Trusts

Charitable Trusts can take different forms, and you can quickly find yourself in a sea of acronyms (CRUTs, CRATs, CLUTs and CRATs). What they all have in common is that they are split-interest trusts with a charitable and non-charitable beneficiary. The most common type are charitable remainder trusts, which pay an income stream that is either fixed (a charitable remainder annuity trust, CRAT) or a fixed percentage of the trust’s fair market value (a charitable remainder unit trust, or CRUT). The income stream from a CRT can either be the donor’s lifetime or a specified time period, though the latter cannot exceed 20 years. Contributions to the trust are partially tax deductible, based on a calculation of the present value of the amount that will eventually pass to charity.

__________________________________________

It should also be noted that these structures can be used in combination with one another. For example, it is possible to have a DAF be the beneficiary of a PIF or charitable trust. That allows for a donor’s heirs to play a more active role in philanthropy beyond the donor’s lifetime.

One of the best things about the work we do is helping our clients share their good fortune with causes they care about. While we hope this paper provides a view of the landscape of various giving structures, we encourage you to talk to your financial, tax and legal advisors to choose the option that is best for you.